What Is a Middle School Age Friendly Definition of Class/socioeconomic Status

This post will look in depth at the average net worth by age for the upper middle class. The upper middle class, aka the mass affluent, is loosely defined as individuals with a net worth or investable assets between $500,000 to $2 million. The upper middle class is also sometimes referred to as the aspirational class or HENRYs.

Some also define upper middle class as those who are college educated with incomes in the top 15%. A top 15% income is roughly $100,000 or greater for households or $65,000 or greater for individuals.

The upper middle class is an aspirational class that many aspire to achieve. With enough hard work, determination, and a long enough life, many of us can achieve upper middle class status.

The upper middle class didn't inherit their money. They mostly earned it through hard work. On the other hand, getting rich with a net worth of above $10 million, often takes a tremendous amount of luck.

The Middle Class Is Different

The middle class is different from the upper middle class. The middle class is defined as those earning between 67% and 200% of the U.S. median household income. The Pew Research Center defines middle-class households as those .1 That's between $42,330 and $126,358, using the U.S. Census Bureau's 2020 median income of all households.

We can also define middle class in terms of net worth. According to the U.S. Census data, the average net worth for U.S. households in 2019 (latest data available) was $299,700. The median net worth was $94,670. I mother words, wealth is concentrated at the top.

The Average Net Worth By Age

To calculate the average net worth for the upper middle class, let's first look at the average net worth of all Americans. This data comes from the US Federal Reserve.

- The average net worth for Americans less than 35: $73,500

- The average net worth for Americans between 35 – 44: $299,200

- The average net worth for Americans between 45 – 54: $542,700

- The average net worth for Americans between 55 – 64: $843,800

- The average net worth for Americans between 65 – 74: $690,900

- The average net worth for Americans 75 or more: $528,100

- The average net worth figures are quite impressive.

The middle class is a fine class. However, let us aspire to get into the upper middle class in our lifetime. After all, we'd all much rather achieve financial freedom sooner, rather than later.

Key takeaways from average net worth by age data:

1) Volatile wealth. There's a huge 37% decline in the average American's net worth for the same period (55-64 to 75+), which may signify that the average American isn't as adept in making their money last into retirement. They are perhaps spending down their principal instead of investing their net worth in stable, income producing assets.

2) The average American starting out is struggling. For the first 35 years, the average American is struggling to make ends meet. They're probably in school, paying off debt, and saving for a rainy day. There's probably a lot of angst about never being able to get financially ahead in such a competitive and expensive world.

3) The average American does well later in life. The average net worth by age in America is actually quite healthy, contrary to popular belief that most Americans don't save enough for retirement. Clearly, extremely wealthy individuals will skew the averages higher. But, the biggest surprise is the $843,800 average net worth figure for the typical American ages 55-64. That's almost like saying everybody who is between the age of 55-64 is a millionaire!

The More Money You Have, The Better

This data should stand out as much as the incredible study which says that 100% of Americans who make more than $500,000 a year are happy. But the media doesn't want to report on positive financial findings because poverty and suffering garners more traffic and advertising dollars.

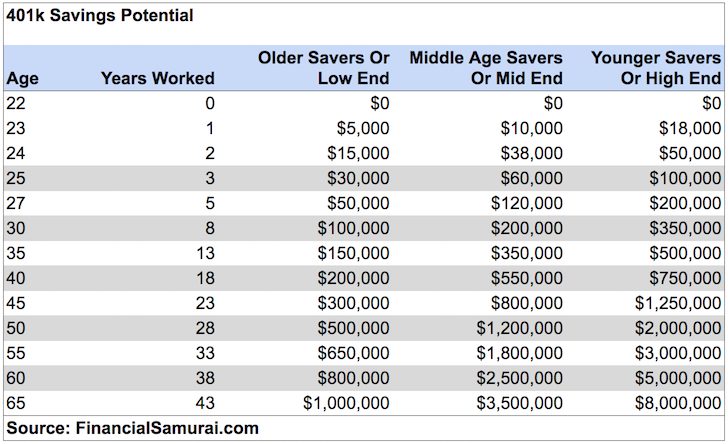

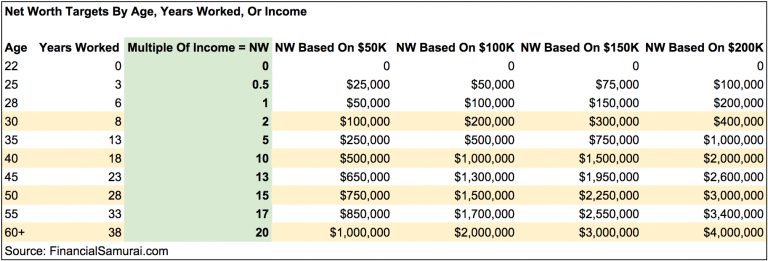

For the average American, their financial lives get so much better later on in life. Perhaps this is why older people are more relaxed, less insecure, and almost all agree with my own average net worth and 401k charts.

I can hear a cacophony of complaints about how absurd the data is by the US Federal Reserve regarding the average net worth by age. Don't worry. I've already got a headache listening.

Averages tend to skew the numbers higher due to a concentration of very wealthy individuals. Therefore, let's take a look at the median and average net worth for Americans according to the Federal Reserve.

Median net worth by age provides for potentially a more realistic picture of the "average" American. The sweet spot for net worth amount continues to be ages 55 – 64, right before the traditional retirement age of 65.

The curve of the median net worth chart, if we were to graph it, looks the same as the average net worth chart. By the time the median American reaches 75+, s/he has spent down 35% of principal.

Let's look on the bright side of things. If you still have $163,100 in median net worth by age 75+, you're probably going to turn out just fine, especially if you have long-term care insurance. Protect your family.

If we add on pensions or Social Security, is the retirement crisis really so bad? None of us have to live in expensive cities such as San Francisco, New York, Honolulu or Los Angeles during our non-working years either. We can hop on a bus to Iowa, Indiana, South Dakota, or Louisiana to allow our net worth to last longer.

For those of you who are really bearish about the financial health of the average American, or who feel upset because your net worth isn't in-line with the upper middle class net worth figures, here's a chart to justify your concerns. The chart below shows that the median US household has gone nowhere in the past 50 years!

Remember, when it comes to data, we can pretty much believe whatever we want to make ourselves feel better. We see what we want to see, in order to justify our actions.

Average Net Worth For The Upper Middle Class

Now that we've analyzed the data for all Americans with averages and medians, let's look at the average net worth for the upper middle class.

The above average person isn't drawing down capital to survive due to their creation of multiple income streams, smart asset allocation, discipline to consistently live within one's means, and the desire to leave money for loved ones and charities who are in dire need of funding. The Financial Samurai ideology is to leave the world better off than when we first entered.

Finally, the financially savvy person understands the estate tax (death tax) doesn't kick in until assets are over $11,700,000 for persons dying in 2021.

Therefore, every single person might as well shoot for accumulating up to $11,580,000 to help other people. But the reality is, anything above $10 million is a top 1% net worth and rich, not upper middle class.

Anything earned beyond such an amount should be spent with great enthusiasm while alive!

Be Careful Having Too Much House

One of the problems with the average American is that the value of their house dominates their net worth. The upper middle class (top 20% of Americans) have a net worth where their primary residence is worth less than 30% of their overall net worth.

Conversely, notice how a house takes up more than 60% of the average American's net worth. Therefore, the average net worth for the upper middle class should have a very diversified net worth.

How To Join The Upper Middle Class

If you want to join the upper middle class per your age group, do the following:

1) Max out your 401k and/or IRA as soon as possible. Try and save an equal or greater amount in after-tax investments as well.

2) Think about the proper asset allocation in relation to personal risk. Your assets should be deployed in a way that aims to beat the risk-free rate of return by at least 2-3X. Stay diversified and never confuse brains with a bull market!

3) Voraciously read as much as possible about wealth management, investing, retirement, taxes, and other issues. Subscribe to the Financial Samurai newsletter for free and other finance sites written by finance veterans. Don't be afraid to seek professional financial help too.

4) Move to a part of the country where there is opportunity. Give yourself a chance to get financially lucky by coming to areas where there is robust employment and brain share. It used to take two months to cross the country. Now it only takes five hours by plane.

5) Buy a home that you can afford and own it for as long as possible. You'll wake up 20 years from now and thank yourself for having something to show for all your monthly payments. Forced savings through principal payments may sound rudimentary, but most people don't have enough discipline to save on a regular basis.

6) Don't be afraid to seek professional financial help if you're lost. Put it this way. The more lost you are, the more bang for your buck you get hiring someone to give you advice or manage your money.

7) Make sure you are properly insured: health, life, auto, house, and umbrella policy. Any number of bad things can happen that can easily wipe away your net worth.

8) Work and invest for as long as possible. "Time in the market is more important than timing the market," as the saying goes. Half the battle is just surviving through all the ups and downs, which is why consistent dollar cost averaging and refining of work skills is important.

9) Once you've properly diversified your wealth, things start getting a little messy. Track your finances through Excel, or a free financial tool by Personal Capital in order to optimize your finances and make sure there aren't any leakages. It's hard to improve what you don't measure.

10) Finally, think positively! If you want to join the upper middle class, believe you deserve to be wealthy. Don't let the government or naysayers keep you down. Use constant failures as learning points. Use rejections as motivation to prove others wrong. There's so much money out there for the taking!

Build Upper Class Wealth Through Real Estate

To achieve an upper middle class net worth, I highly recommend investing in real estate in addition to stocks. If you look at the average net worth by age for the upper middle class, real estate is a core component to the net worth composition. Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties.

Given interest rates have come way down, the value of rental income has gone way up. The reason why is because it now takes a lot more capital to generate the same amount of risk-adjusted income. Yet, real estate prices have not reflected this reality yet, hence the opportunity.

My two favorite ways to invest in real estate are through:

Fundrise: A way for accredited and non-accredited investors to diversify into real estate through private eREITs. Fundrise has been around since 2012 and has consistently generated steady returns, no matter what the stock market is doing. For most people, investing in a diversified real estate fund is the easiest way to go.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations, higher rental yields, and potentially higher growth due to job growth and demographic trends. You can build your own select real estate fund with CrowdStreet.

Both platforms are free to sign up and explore.

I've personally invested $810,000 in real estate crowdfunding across 18 projects to take advantage of lower valuations in the heartland of America. The upper middle class are big investors in real estate to benefit from rent increases and property price increases.

Due to my real estate investments since 2003, I've been able to handily achieve a net worth far above the average net worth by age for the upper middle class. The key to building great wealth is through aggressive saving and savvy investments. Real estate is a proven wealth-builder long term.

FinancialSamurai.com was started in 2009 and is one of the most trusted personal finance sites today with over 1.5 million organic pageviews a month. Financial Samurai has been featured in top publications such as the LA Times, The Chicago Tribune, Bloomberg and The Wall Street Journal. Sign up for my free weekly newsletter here.

What Is a Middle School Age Friendly Definition of Class/socioeconomic Status

Source: https://www.financialsamurai.com/the-average-net-worth-by-age-for-the-upper-middle-class/

{kind=link}

Post a Comment for "What Is a Middle School Age Friendly Definition of Class/socioeconomic Status"